Let’s be honest.

“Battery storage” doesn’t sound like the most exciting topic in the world.

But here’s the part most people miss:

It’s the technology that decides whether your city stays powered during a blackout… Whether solar and wind can actually replace fossil fuels… And which countries control the future of energy.

That’s not a niche story.

That’s a system-level shift.

And in 2026 — it’s accelerating fast.

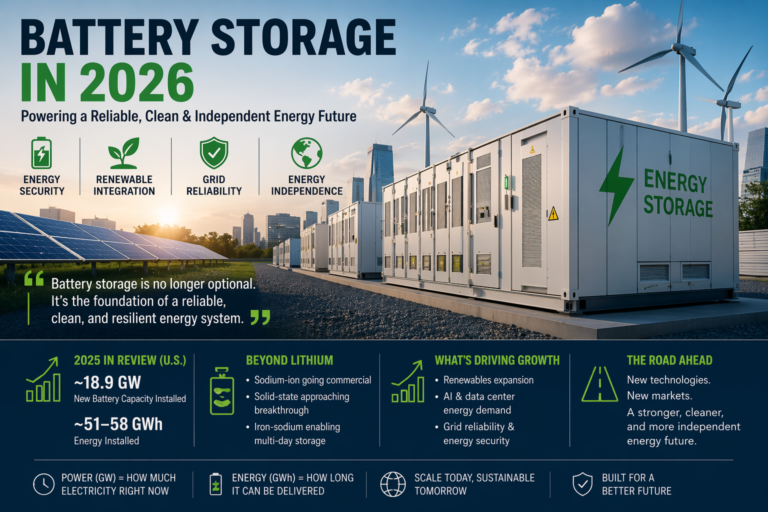

The Big Picture: Why Everyone Is Suddenly Paying Attention

For years, battery storage was the background player.

Solar panels and wind turbines got the spotlight. Batteries quietly did their job behind the scenes.

But here’s where things changed.

Renewable energy scaled faster than the grid could handle.

On sunny afternoons, solar produces more power than we can use. Without storage, that energy gets wasted — or systems have to shut down production.

Now pause and think about that.

We are literally generating clean energy… and throwing it away.

That’s the problem batteries solve.

And once that problem became obvious, everything shifted.

Here’s how fast things moved:

In 2024, the U.S. installed approximately 10 gigawatts (GW) of utility-scale battery storage — a record at the time.

By the end of 2025, the U.S. had added approximately 18–19 GW of new battery capacity — nearly double the 2024 record, with total energy installed estimated at 51–58 GWh for the year.

Quick note on the numbers: GW (gigawatts) measures power — how much electricity can be delivered at once. GWh (gigawatt-hours) measures energy — how long that power can be sustained. Both matter. A battery that can deliver 1 GW for only minutes isn’t very useful. A 1 GWh system running for four hours is.

That’s not incremental growth.

That’s a structural shift.

The Technology Race: It’s No Longer Just Lithium

For a long time, lithium-ion batteries dominated everything.

Phones. Laptops. Electric vehicles. Grid storage.

But now — for the first time — real alternatives are emerging.

And this is where things get genuinely interesting.

Because this isn’t one race.

It’s multiple races happening at once.

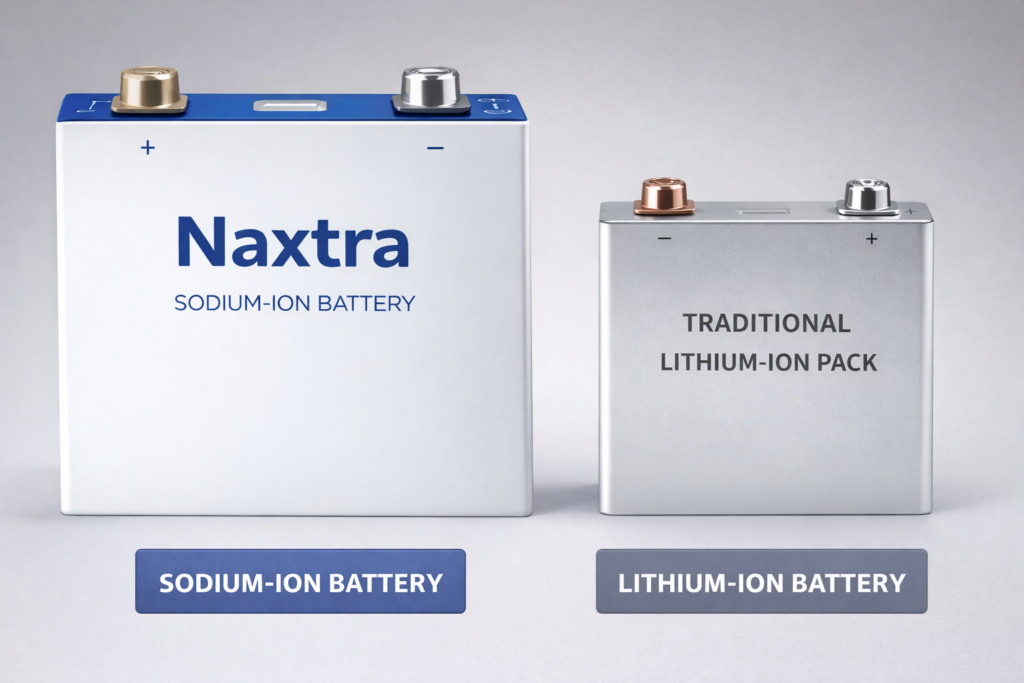

Sodium-Ion: The “Simple” Idea That Changes Everything

Sodium-ion vs lithium-ion battery size and structure comparison

Here’s a surprising fact.

Sodium-ion batteries work almost the same way as lithium-ion.

The only difference?

They use sodium instead of lithium.

As in — salt.

That matters more than it sounds.

Because lithium is:

- limited in supply

- geopolitically sensitive

- concentrated in a few mining countries

Sodium is:

- abundant everywhere

- cheap to source

- free from geopolitical strings

Now add this:

Companies are no longer just testing sodium-ion.

They are deploying it at scale.

CATL — the world’s largest battery manufacturer — confirmed commercial rollout of sodium-ion across passenger vehicles, commercial vehicles, battery swap systems, and energy storage in 2026. Their Naxtra product line is already in production, reaching 175 Wh/kg energy density — enough for a 500-kilometer EV range — and has passed China’s national battery safety standard.

BYD is right behind, developing sodium-ion with up to 10,000 charge cycles for long-life applications, while running sodium-ion and lithium-ion development in parallel.

In the U.S., companies like Natron Energy and Peak Energy are deploying sodium-ion systems at grid scale domestically — arguing that sodium-ion “doesn’t just solve a cost issue, it solves a risk issue.”

That’s the moment a technology stops being “interesting”…

And starts being inevitable.

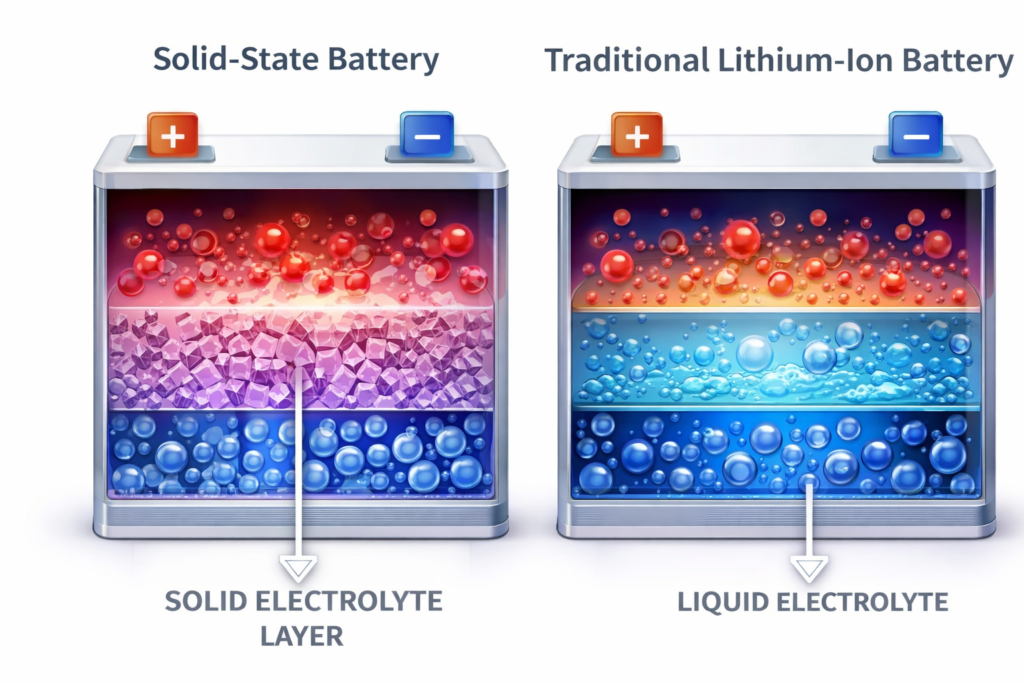

Solid-State Batteries: The Big Prize (But Not Quite Yet)

Solid-state vs lithium-ion battery: comparison of solid electrolyte and liquid electrolyte structures

If sodium-ion is the near-term shift…

Solid-state is the long-term breakthrough.

The concept is straightforward:

Replace the liquid electrolyte inside batteries with a solid material.

The result?

- Higher energy density

- Longer lifespan

- Safer — no flammable liquid to worry about

But here’s the honest reality.

Building this at commercial scale is extraordinarily difficult.

BYD’s chief scientist recently stated that solid-state batteries have entered a “critical breakthrough stage” — while also noting that commercialization remains constrained by engineering complexity, cost control, and production yield challenges. Core bottlenecks include solid-solid interface stability and lithium dendrite suppression at the material level.

Translation: researchers are solving the hardest problems. Manufacturing them reliably at millions of units is a separate challenge entirely.

Most credible timelines point to 2027–2028 for initial commercialization across premium vehicle segments.

The hype is real. The impact is still a couple of years away.

Iron-Based Long-Duration Storage: The Underrated Breakthrough

This one sounds almost too simple to be real.

Some next-generation batteries work by exploiting the chemistry of iron — including the basic process of rusting.

When the battery discharges, the iron oxidizes (rusts). When it charges, the process reverses. Repeat for 7,000 cycles over 20 years.

A quick note on terminology: companies like Inlyte Energy are building iron-sodium batteries — a specific chemistry combining sodium and iron — which is different from the “iron-air” concept (which uses atmospheric oxygen). Both are promising; Inlyte’s approach is already at field-test stage.

Why does this matter?

Because iron is:

- extremely cheap

- widely available

- non-flammable

And crucially — these batteries can store energy for days, not hours. That’s something lithium-ion can’t economically do at scale.

Inlyte proved out their full-scale iron-sodium system in factory testing with 83–90% round-trip efficiency, projecting a battery life of at least 7,000 cycles or 20 years at a fraction of the cost of comparable systems. Field installation is underway at Southern Company’s Energy Storage Test Site in Alabama, with U.S. manufacturing planned for 2026.

This isn’t a replacement for lithium-ion.

It’s a solution for a different problem — multi-day grid backup — that lithium-ion was never designed to solve.

And that’s exactly what a diversifying energy storage market needs.

What’s Actually Being Built Right Now

Technology is one thing.

Deployment is what really matters.

And here’s the encouraging part: a lot is already happening — across more regions and use cases than most people realize.

Texas and the U.S. Grid: More Than One Project

Texas has become one of the world’s most active markets for large-scale battery deployment, driven by the ERCOT grid’s exposure to extreme weather events and its high renewable penetration.

North America’s largest grid-scale hybrid energy storage facility — a 1.2 GWh project pairing flow battery technology with lithium-ion systems — completed full commissioning in Texas in early 2026.

But Texas is just the headline.

Across the U.S., utility-scale battery storage is showing up in every region. California, Arizona, Florida, and the Southeast are all adding significant capacity. The Sacramento Municipal Utility District, for example, is building a 160 MW / 640 MWh battery system on a decommissioned nuclear plant site — old energy infrastructure making way for the new.

That geographic spread matters. The U.S. battery storage buildout is no longer concentrated in one state or one use case. It’s national infrastructure now.

Florida & Arizona: Storage as a Community Resource

Battery systems are being deployed specifically for underserved communities and emergency resilience in ways that weren’t happening even three years ago.

In Tallahassee, a $39 million battery project backed by a $28.7 million DOE grant will serve historically underserved neighborhoods — ensuring grid resilience reaches the communities that have historically been last in line for infrastructure upgrades.

In Tempe, Arizona, a $20 million Resilience Hubs Microgrid Program will add solar, battery storage, and islanding controls to city resilience centers — allowing them to operate independently during outages, providing cooling, food storage, and essential services when the main grid goes down.

Battery storage isn’t just a technology trend.

It’s becoming community infrastructure.

Europe: A €5 Billion Strategic Bet

The European Commission formally approved a €5 billion Energy Storage Accelerator package in early 2026, covering utility-scale battery deployments, long-duration energy storage research, and a pan-European battery recycling network.

But make no mistake — this is as much about geopolitics as it is about climate.

The EU is explicitly trying to reduce strategic dependence on concentrated global supply chains — which means reducing dependence on China, which currently dominates battery cell manufacturing, raw material processing, and key component supply at almost every level of the value chain.

Building a domestic European battery stack, from mining to manufacturing to recycling, is a decade-long project. The €5 billion is the starting gun.

The AI Factor: The Demand Driver Nobody Predicted

Here’s a development that barely registered as a story two years ago:

AI is creating a massive new source of electricity demand.

Data centers running large AI workloads consume enormous amounts of power — and that demand is growing faster than the grid can accommodate. Companies are facing multi-year interconnection queues just to get power access for new facilities.

So they’re turning to batteries.

Not as backup. As a primary solution for co-locating generation and storage near where they need power — without waiting years for utility infrastructure to catch up.

Google has already invested in long-duration energy storage specifically to address surging AI data center power demand. Other hyperscalers are making similar moves.

Battery storage now has a new and very large customer: the AI industry.

And this demand is only growing — driving particular interest in flow batteries and other non-lithium, non-flammable chemistries that handle the constant high-frequency cycling of data center operations better than standard lithium-ion.

The Reality Check: Real Challenges Exist

Not everything is smooth.

The tariff problem is real.

Since early 2025, battery storage costs have risen 56–69% due to the Trump administration’s tariff policies on imported components. New Foreign Entity of Concern (FEOC) regulations, kicking in fully in 2026, add further complexity — restricting which battery components qualify for federal tax credits based on country of origin.

The intent is sound: reduce strategic dependence on Chinese manufacturing for critical infrastructure. But the short-term effect is that projects cost more and take longer to finance.

Supply chains are still deeply integrated with China.

The global battery ecosystem — raw materials, cell production, inverters, battery management systems — runs through Chinese manufacturing at almost every level. Rebuilding that domestically takes years and billions of dollars.

The honest assessment:

This is short-term pain driving long-term structural change. The U.S. and Europe are serious about domestic manufacturing — the investment, the regulations, and the policy architecture all point in the same direction. But the transition period is genuinely difficult for project developers right now.

The Investment Picture: Growing Up Fast

The investment trend tells an interesting story about where this market is in its development cycle.

After a record 2024 — approximately $19.9 billion invested across roughly 116 energy storage financing transactions — capital became more disciplined in 2025. Investors shifted toward quality over volume: fewer deals, more focus on de-risked assets, preference for later-stage projects with contracted revenues and proven technology.

That’s a healthy signal. It means the market has graduated from early hype to execution-focused maturity.

Institutional infrastructure is being built alongside it. The NSF Energy Storage Engine in upstate New York received $45 million for Phase 2, matched by $16 million from New York State — supporting battery startups, industry-academia research teams, and the Northeast’s first advanced battery safety testing facility at Rochester Institute of Technology. The ambition: make upstate New York America’s battery tech capital.

Key Stats at a Glance

| Metric | Number | Context |

| U.S. battery storage added in 2025 | ~18–19 GW / 51–58 GWh | Nearly double the 2024 record |

| CATL sodium-ion energy density | 175 Wh/kg | Sufficient for 500km EV range |

| Texas hybrid BESS capacity | 1.2 GWh | North America’s largest hybrid project |

| EU Energy Storage Accelerator | €5 billion | Utility-scale, LDES, recycling network |

| U.S. cost increase from tariffs | 56–69% | Key near-term challenge for developers |

| Inlyte iron-sodium efficiency | 83–90% round-trip | Projected 7,000 cycles / 20-year life |

| Investment in storage 2024 | ~$19.9 billion | Record; 2025 more selective but steady |

| NSF Energy Storage Engine Phase 2 | $45M + $16M state match | Battery R&D and workforce, upstate NY |

Five Things to Watch for the Rest of 2026

Let’s simplify everything into what actually matters next:

1. CATL’s sodium-ion delivery. Will the commercial rollout happen on schedule, and what do real-world performance numbers look like outside controlled testing environments?

2. Solid-state timelines. Do the 2027–2028 commercialization targets hold? Watch for early production data from pilot lines.

3. FEOC compliance and domestic manufacturing. As sourcing rules bite harder in H2 2026, which companies adapt fastest — and can U.S./European manufacturing actually scale to fill the gap?

4. AI-energy storage deals. The first major long-term contracts between hyperscalers and battery storage developers will set the template for what could become one of the largest new markets in the industry.

5. Europe’s execution. The €5 billion is committed. Now watch which projects get funded first, how quickly capacity builds, and whether European cells can close the cost gap with Chinese imports.

Conclusion: Why This Matters More Than Most People Realize

Here’s the simplest way to understand battery storage:

It makes everything else work.

Without storage:

- Solar is intermittent

- Wind is inconsistent

- Grids become harder to balance as renewables grow

With storage:

- Energy becomes flexible, reliable, and dispatchable

- Renewables can replace fossil fuels without sacrificing reliability

- Grids can absorb clean energy surpluses and deliver them when demand peaks

That’s the shift happening right now.

This is not just a technology trend.

It’s infrastructure. It’s geopolitics. It’s economics. It’s the foundation of the next energy system.

And the most important part?

This transition is not coming.

It’s already underway.

Final Thought

The question is no longer: “Do batteries matter?”

That answer is settled.

The real question is:

Who controls the technologies, supply chains, and systems that power the next generation of energy?

Because whoever does — controls a significant part of the future.

The race is already underway.

And 2026 is when it stopped being theoretical.

Further Reading & Sources

- IEA Energy Storage Tracker — iea.org — Global deployment data, updated quarterly

- Energy-Storage.News — energy-storage.news — Project news, technology analysis, market intelligence

- MIT Technology Review — Sodium-Ion Batteries — technologyreview.com — Accessible explainer on sodium-ion’s commercial momentum

- CATL / Naxtra — catl.com — World’s largest battery manufacturer; sodium-ion product line

- Inlyte Energy — inlyte.energy — Iron-sodium long-duration storage, U.S. manufacturing

- PV Magazine Energy Storage — pv-magazine.com — Deep coverage of policy, finance, and battery technology