Something remarkable is happening in tech right now.

For the last few years, most of Silicon Valley has been focused on chatbots and large language models. But at the same time — quietly at first, and now very visibly — billions of dollars have started flowing into a different kind of AI.

Not the kind that just answers questions.

The kind that moves, lifts, drives, and works in the real world.

Robotics funding in 2026 isn’t just growing — it’s redefining what investors believe is possible. From a massive $16 billion raise for a self-driving company to startups doubling their valuation in months, the scale and speed of capital entering this space is something we haven’t seen before.

If you want to understand where technology is actually heading — not just online, but in the physical world — this is the shift to watch.

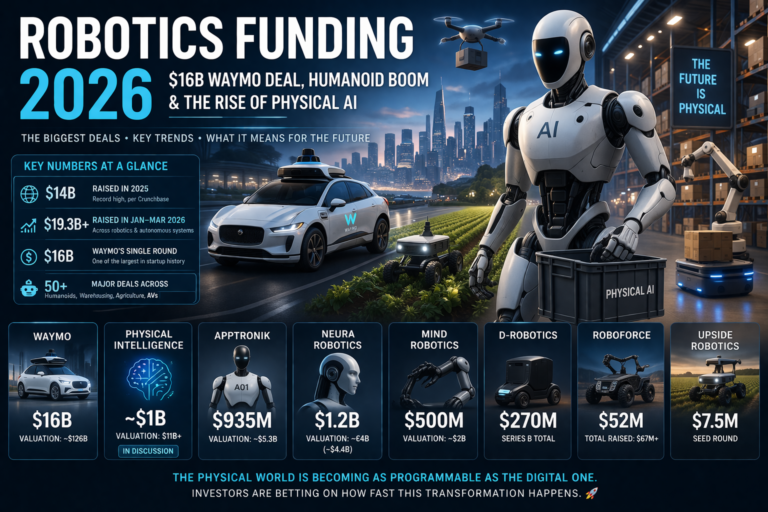

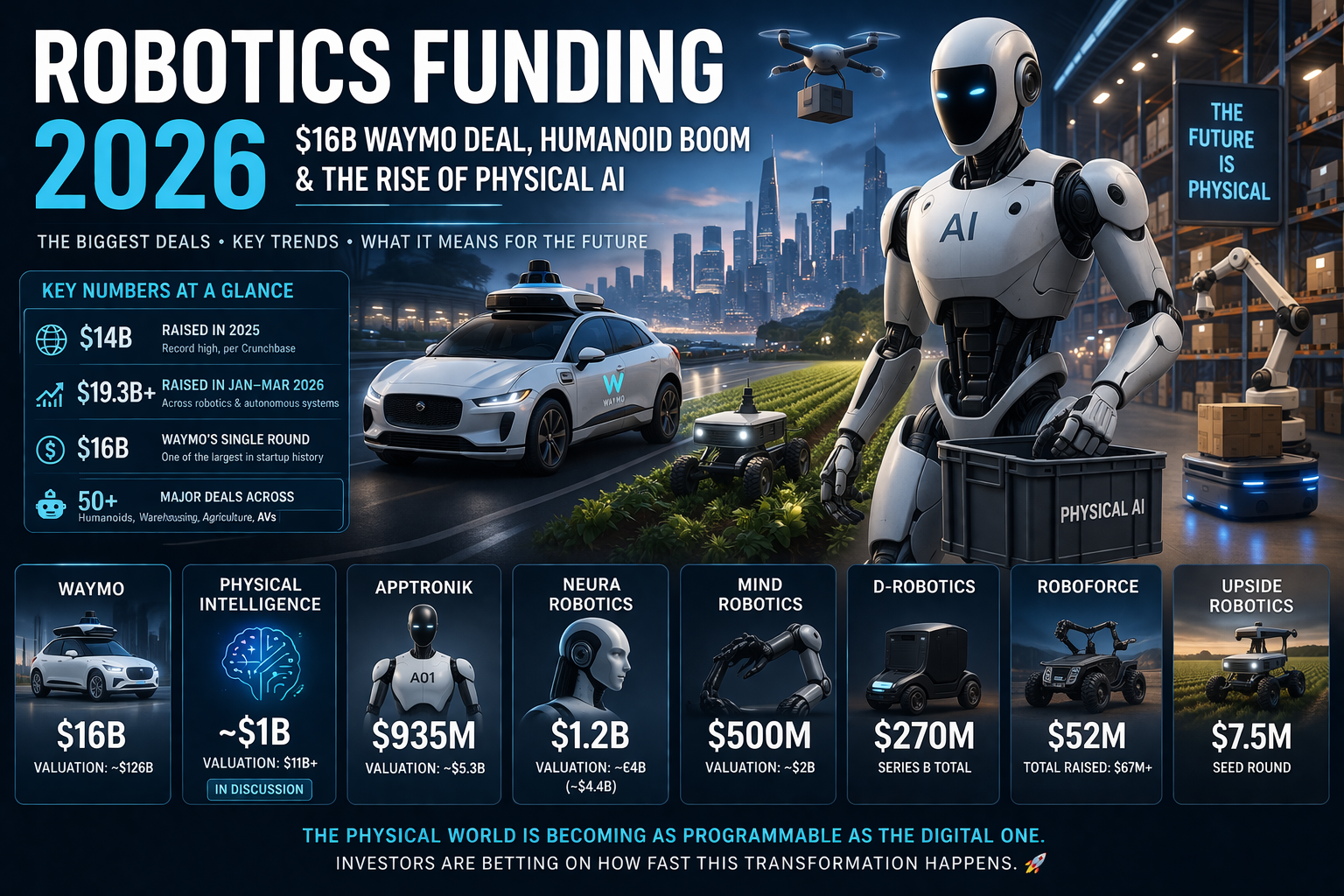

Key Numbers at a Glance — Robotics Funding 2026

- $14 billion raised by robotics startups globally in 2025 (record high, per Crunch base)

- $19.3B+ raised across robotics and autonomous systems in Q1 2026 alone

- $16B — Waymo round, one of the largest startup raises in history

- $935M — Apptronik Series A (~$5.3B valuation, Apollo humanoid robot)

- ~$1B — Physical Intelligence round in discussion (~$11B+ valuation, general-purpose robot AI)

- $1.2B — Neura Robotics raise (~€4B / ~$4.4B valuation, teach-by-demonstration robots)

- $500M — Mind Robotics (~$2B valuation, factory AI robots backed by Rivian)

- $270M — D-Robotics Series B (embodied AI infrastructure, China)

- $52M — RoboForce (industrial Physical AI for harsh environments)

- $7.5M — Upside Robotics (autonomous fertilizer robots, Tier-1 VC backed)

- $11.8B — Total Bay Area AI robotics VC since 2020, per PitchBook

What makes these numbers genuinely significant isn’t just the totals. It’s how wide the funding is. This isn’t one hot company or one hot category. It’s an entire ecosystem – humanoids, warehouse robots, agricultural automation, industrial AI, inspection drones — being funded at the same time, across every stage from $7.5M seed rounds to $16B mega-closes. That breadth is the real story.

Why Robotics Funding Is Exploding Right Now

The AI Moment Has Finally Reached the Physical World

For years, AI mostly lived in software. It could write, analyze, and recommend but it didn’t act in the real world.

Now it does.

Robots are learning how to pick up objects, navigate unpredictable spaces, drive vehicles, and operate in messy real-world environments. That shift from digital intelligence to physical capability is what’s unlocking this funding wave. Foundation models, the same class of AI behind today’s chatbots, can now be fine-tuned to operate physical hardware. Robots that once needed exhaustive reprogramming for every new task can now learn through demonstration. That’s a fundamental change in what’s possible.

Labor Shortages Are Creating Real Demand

This isn’t just a technology trend it’s a business necessity.

Industries like manufacturing, logistics, agriculture, and construction are all facing serious labor shortages, especially for work that is repetitive, physically demanding, or outright dangerous. That creates genuine commercial pull that didn’t exist in earlier robotics hype cycles. Companies aren’t funding robots because the technology is cool. They’re funding them because they need them.

Strategic Investors Are Moving Fast and That Signals Something

Look at who is actually writing the checks: Mercedes-Benz, John Deere, NVIDIA, Uber, Volvo, AT&T Ventures, Google, and Qatar Investment Authority.

These aren’t passive financial bets. These are industrial companies positioning themselves for a future where physical AI is embedded in their core operations — from factory floors to logistics networks to transportation infrastructure. When the world’s largest manufacturers start funding the robots they plan to deploy, the adoption timeline compresses fast.

The Biggest Robotics Funding Rounds of Q1 2026

1. Waymo — $16 Billion

This is the deal that reset expectations for the entire sector.

Waymo raised $16 billion at a reported ~$126 billion valuation co-led by Dragoneer, DST Global, and Sequoia, with Andreessen Horowitz, Mubadala, and Silver Lake among the participants. It ranks among the largest startup raises in history.

But the real story isn’t the size. It’s the stage.

Waymo is already running a commercial robotaxi service at scale, completing hundreds of thousands of rides per week across U.S. cities. London and Tokyo launches are planned for 2026 through a partnership with Uber. This round isn’t funding a prototype it’s funding geographic expansion of a product that is already operational. That is what physical AI looks like when it moves beyond testing and starts becoming infrastructure.

One important context note: autonomous mobility (robotaxis and self-driving trucks) accounts for over $18 billion of the $19.3 billion raised across robotics and autonomous systems in Q1 2026. Waymo alone drives most of that figure. Strip it out, and the underlying robotics market — humanoids, warehouse automation, industrial AI, agrotech is still running at a multi-billion dollar annual pace. The Waymo number is a signal, not a distortion.

2. Physical Intelligence ~$1 Billion

Physical Intelligence is moving at a pace that makes even experienced investors stop and look twice.

Founded just two years ago by researchers from Google DeepMind and top AI labs, the company raised $600M at a $5.6B valuation and is now reportedly in talks for another ~$1B round that could value it above $11B. That would be a near-doubling in valuation in under four months.

What investors are betting on here isn’t a single product. It’s a platform.

PI is building general-purpose AI models for robots the kind that can power many different robot types across many different tasks. If that works, the company doesn’t just build one successful robot. It becomes the infrastructure layer the entire robotics ecosystem runs on. That’s the magnitude of the bet, and it explains the valuation velocity.

3. Apptronik — $935M Series A

If there’s one company that best represents the shift from “humanoid robots are a science project” to “humanoid robots are a real business,” it’s Apptronik.

Its Apollo robot is a full-sized bipedal machine built for warehouses and factories — doing the physically demanding work that labor shortages are making harder and harder to staff with humans. The company has now raised over $935M in total Series A funding, with Google, Mercedes-Benz, and B Capital joined by strategic investors including John Deere, AT&T Ventures, and the Qatar Investment Authority — all coming in at a 3x valuation multiple from the original raise.

Commercial partnerships with GXO Logistics, Mercedes-Benz, and Jabil are already in place. A strategic tie-up with Google DeepMind powers the robot’s AI through Gemini Robotics. Industrial pilots are running through 2026, with broader scaling expected in 2027 and beyond.

Funding plus partnerships plus real deployments already underway. That combination is what makes this serious.

4. Neura Robotics ~$1.2 Billion

Neura Robotics is building humanoid robots with a strong focus on making them genuinely usable by the companies that buy them.

The standout capability is its teach-by-demonstration approach: instead of requiring engineers to rewrite code for every new task, operators can physically guide a robot through a motion and it learns. That sounds simple. It’s actually a significant deployment advantage. It means shorter setup times, faster adaptation to new tasks, and lower technical barriers for non-specialist users.

The German company is now raising ~$1.2B at roughly a €4 billion (~$4.4B) valuation, backed by stablecoin issuer Tether Holdings. Its prior round was backed by Volvo Cars Tech Fund, and it has already used capital for acquisitions buying ek Robotics GmbH, a 300-person industrial automation specialist. Neura’s momentum is a clear signal that European humanoid robotics is real, funded, and moving fast.

5. Mind Robotics $500 Million

Mind Robotics has an advantage most robotics startups spend years trying to build from scratch: immediate access to real-world manufacturing data at scale.

Backed by Rivian and founded by Rivian CEO RJ Scaringe, the company uses Rivian’s engineering talent and live production data from its Normal, Illinois plant as a training environment for its robots. That built-in data flywheel training AI on real factory conditions rather than simulations gives Mind Robotics a meaningful edge in developing robots that actually work reliably in production settings. The $500M raise from Accel and Andreessen Horowitz, at a ~$2B valuation, brings total funding to over $600M.

6. D-Robotics $270 Million

D-Robotics is the company building the infrastructure that other robots will run on.

Spun out of autonomous driving chipmaker Horizon Robotics, the company develops computing platforms and general-purpose hardware/software infrastructure for embodied AI. Think of it as the chipmaker and platform layer of the robotics ecosystem the kind of company that becomes more valuable as everything above it grows. Its recent growth confirms the thesis: shipments up 180%, customer base up 200% year-over-year. The $270M Series B — backed by Didi Global, Prosperity7, GL Ventures, and 5Y Capital — is funding global expansion and deeper edge-cloud integration.

7. RoboForce $52 Million

RoboForce operates at the hardest end of the industrial robotics market: solar farms, mining operations, data centers, shipping facilities — environments that are genuinely dangerous, physically demanding, and chronically understaffed.

The company calls its model “Robo-Labor,” and the framing is accurate. These are robots deployed specifically to take over the dull, dirty, and dangerous work that creates the highest human cost when it goes wrong. Founded by alumni from CMU, Amazon Robotics, Google, Waymo, and Tesla Robotics, RoboForce is building its AI stack on NVIDIA’s infrastructure (Jetson Thor + Isaac Sim) and raised $52M in an oversubscribed round led by YZi Labs. For anyone tracking where mid-stage industrial robotics capital is going, this is a useful benchmark.

Beyond the Mega-Rounds: Mid-Stage and Niche Deals That Signal Ecosystem Depth

The biggest rounds tell one part of the story. But the ecosystem’s true health shows up at smaller sizes and in less obvious categories.

Warehouse picking: Nomagic, which builds AI-driven picking robots for distribution centers, closed a round in Q1 2026 alongside several competitors. The warehouse picking market remains fragmented — no single platform dominates — but consistent capital flow into the segment confirms it as a durable commercial category.

Drone-based inventory: Gather AI deploys autonomous drones to scan and locate warehouse inventory from above, feeding live data to management systems. The use case is narrow but highly valuable — inventory accuracy is a persistent pain point for logistics operators, and aerial automation solves it without disrupting ground-level operations.

Agriculture: Upside Robotics, a Canadian startup building autonomous fertilizer robots, closed a $7.5M seed round led by Plural, a Tier-1 European VC that rarely moves at seed stage in agrotech. The fact that a fund of Plural’s caliber led this round signals that agricultural robotics is attracting serious institutional attention — not just niche interest.

Inspection robotics from India: Armatrix (snake-arm robots for confined spaces) and Octobotics (AI-enabled non-destructive testing) both raised rounds within weeks of each other in early 2026, targeting industrial asset inspection across India, Southeast Asia, and the Middle East. These are revenue-generating companies solving real infrastructure safety problems in rapidly industrializing markets — a category rarely covered in mainstream robotics coverage but steadily building out real commercial operations.

Five Key Trends Shaping Robotics Funding in 2026

Trend 1: Humanoids Have Become a Serious Asset Class

Not long ago, humanoid robots felt like a research project. Today they are attracting billions in institutional capital — and more importantly, they are being deployed in real commercial environments. The conversation has shifted from “will this work?” to “how fast can this scale?” That’s not a small shift. It’s a category maturing in real time.

Trend 2: Strategic Investors Are Treating Robotics as Core Infrastructure

Companies like Mercedes-Benz and John Deere are not investing for financial returns alone. They are securing positions in the supply chains and technology platforms that will define their industries over the next decade. When the buyers of robots start funding the makers of robots, adoption timelines compress dramatically.

Trend 3: This Is Becoming a Global Competition

The Bay Area still leads in total AI robotics VC — $11.8B since 2020, nearly 30% ahead of second-place Los Angeles. But Germany produced the Neura Robotics raise. China’s D-Robotics closed a $270M Series B. India generated two inspection robotics rounds in the same month. The U.S. advantage in this space is real, but it is not permanent.

Trend 4: Defense Spending Is Accelerating Commercial Capability

The Pentagon allocated $13.4 billion for autonomous systems in its fiscal 2026 budget. That capital funds durability research, navigation in unstructured environments, and autonomy at a level no commercial company can afford independently. Those advances don’t stay in defense — they flow into commercial robotics over time, compressing the capability curve for everyone.

Trend 5: AI Is the Real Engine Behind All of It

Without better AI, robots remain rigid, expensive, and limited to narrow preprogrammed tasks. With better AI — specifically, foundation models that can be fine-tuned for physical systems — they become adaptable, trainable, and deployable at scale. Every major funding trend in 2026 robotics traces back to this single unlock. The hardware is the vehicle. The AI is the driver.

Challenges the Sector Still Needs to Solve

The opportunity is real. So are the obstacles.

Hardware cost remains the biggest barrier to mass deployment. A humanoid robot priced at $100,000+ per unit serves only a narrow range of high-value industrial use cases. Reaching the cost points required for healthcare or consumer deployment will require manufacturing scale that most companies are still years away from achieving.

Supply chains for actuators and sensors create a less-discussed but equally real bottleneck. High-torque actuators, force-torque sensors, and depth cameras — the physical core of any capable robot — are still produced at relatively low volumes by a small number of manufacturers. As the industry scales, component availability will constrain production speed.

Energy consumption limits operational efficiency. Current battery technology means many mobile robots cannot sustain a full industrial shift on a single charge. Until power density improves significantly, duty cycles remain a real constraint on where and how robots can be deployed.

Reliability in unstructured environments is still hard. Controlled lab performance rarely transfers cleanly to real warehouses, construction sites, or outdoor environments. This is fundamentally an AI problem — and the reason so much capital is flowing toward foundation model companies rather than just hardware makers.

Regulation is largely undefined. As humanoid robots enter workplaces and eventually homes, liability frameworks, safety certification standards, and data privacy rules will need to develop. Companies that build compliance infrastructure early will have a significant advantage over those that treat it as an afterthought.

Talent is scarce. The combination of deep robotics engineering, modern AI capability, and manufacturing operations experience is rare and intensely competed for. Every company raising large rounds is simultaneously fighting for the same small pool of people who can actually build what has been promised.

Conclusion: The Physical AI Era Has Begun — and the Clock Is Running

This isn’t just a funding trend.

It’s a shift in how the world works.

Yes, Waymo’s $16 billion round grabs headlines. But the deeper signal is everything happening around it — humanoid robots entering real workplaces, AI platforms being built to power entire robot ecosystems, industrial automation scaling globally, and new markets emerging across Europe, Asia, and emerging economies simultaneously.

The physical world is starting to become programmable — just like software did.

And the investors writing billion-dollar checks in 2026 are not asking if this happens anymore.

They have already decided it will.

The only question left on the table is execution: which companies build reliably, deploy at scale, and earn the trust of the industries they serve. That race is already underway. And unlike software, where pivoting is cheap, the winners here will be built on hardware, supply chains, and real-world deployments that take years to replicate.

The window to position — as a company, an investor, or an enterprise buyer — is open now. It will not stay open indefinitely.